13 Minutes

13 Minutes

Key Takeaways

- Homeowners across the U.S. and EU are adjusting their spending habits in response to higher mortgage rates. Luxuries, travel, and entertainment are taking a hit, with over 80% cutting back. More than 60% are dipping into savings or working extra hours to cover expenses. Major financial decisions, like buying a car or investing, are being postponed—especially in the U.S.

- As mortgage rates rise, confidence in banks and financial institutions is falling, with 60–70% of homeowners expressing reduced trust. If financial institutions don’t step in with supportive measures, consumers may look elsewhere for financial solutions.

- The economic strain from rising mortgage rates isn’t just about money—it’s impacting people’s well-being. Anxiety, stress, and feelings of powerlessness are common, with many struggling to maintain their quality of life.

In this Article

Money makes the world go round—but in the EU, bank lending keeps things moving. Whether it’s buying a home, launching a business, or making a big purchase, loans are a huge part of everyday life.

By late 2023, loans accounted for over 70% of GDP in most EU member states. In countries like Denmark, Sweden, France, Spain, and the Netherlands, the value of loans even exceeded the size of their entire economies. Mortgages and business loans made up 63% of all bank assets in 2024, showing just how critical they are to the region’s financial stability. (Source: European Central Bank – ECB)

In the US, the numbers tell a similar story. Total mortgage loan balances hit $12.25 trillion in Q4 2023. Despite rising rates and high home prices, the housing market remains central to the economy. By Q3 2024, American households held $34.9 trillion in real estate equity – 72.4% of all residential real estate value. This marks a $2.5 trillion increase from the previous year, even with a $400 billion dip compared to the previous quarter. Housing continues to reflect and shape the broader economic picture. (Source: Lending Tree 2025)

Our latest Sago Omnibus Findings

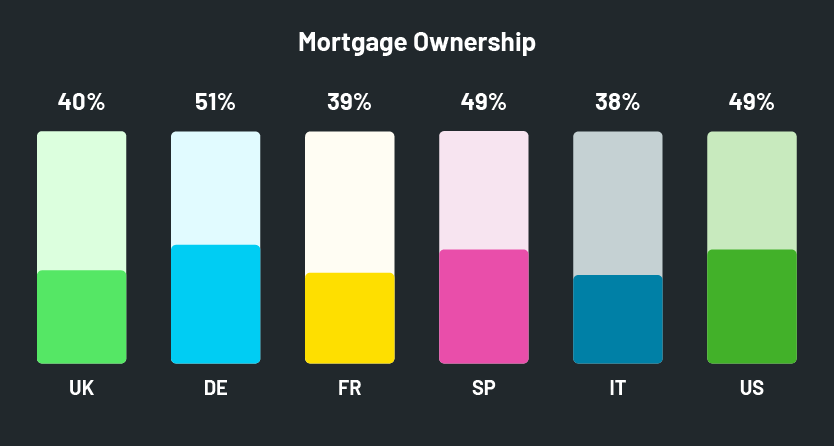

In November 2024, an Omni was conducted amongst 5 EU countries as well as the US. Of the 7613 panel members, 44% are current mortgage owners. Some slight differences per country were noted:

While most have felt the impact of rising rates over the past 12 to 18 months, they’ve managed to adapt. But not everyone has had the same experience. Homeowners in France reported the least impact across the 6 markets, likely due to long-term fixed mortgage rates and flexible financing options offered by institutions and the government. This stability has helped shield them from short-term fluctuations.

However, roughly one-third of all mortgage owners generally had to make some or other trade-off, across the board.

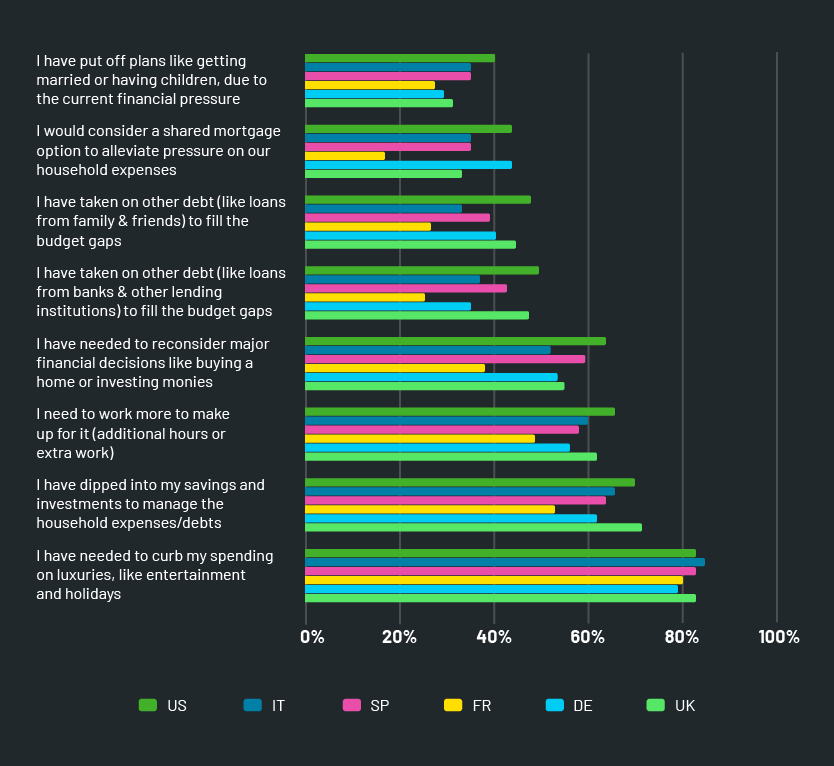

Behavioral Shifts in Response to Rising Mortgage Rates

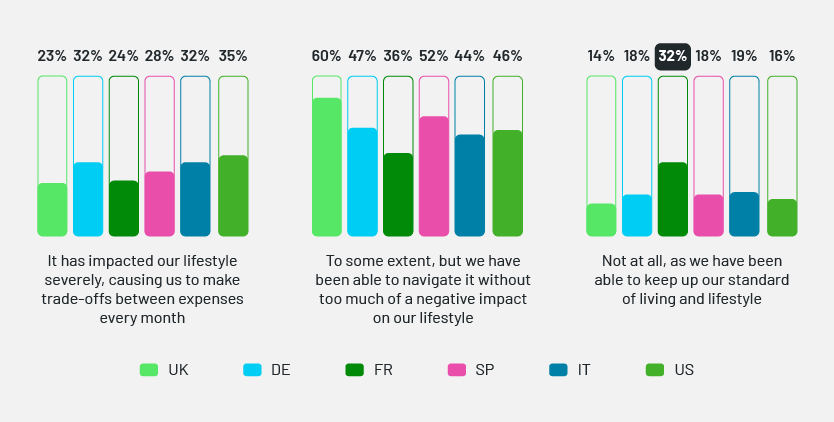

Rising mortgage rates aren’t just affecting monthly payments—they’re reshaping respondents’ spending habits in a big way.

Across all markets, spending on luxuries, entertainment, and holidays took the hardest hit, with over 80% of respondents cutting back in these areas.

More than 60% had to dip into their savings or investments just to keep up with household expenses. And in the US and UK, a significant number of people picked up extra hours at work to make ends meet.

Making major financial decisions (like buying a car or investing) has also needed to take a backburner for now, especially in the US.

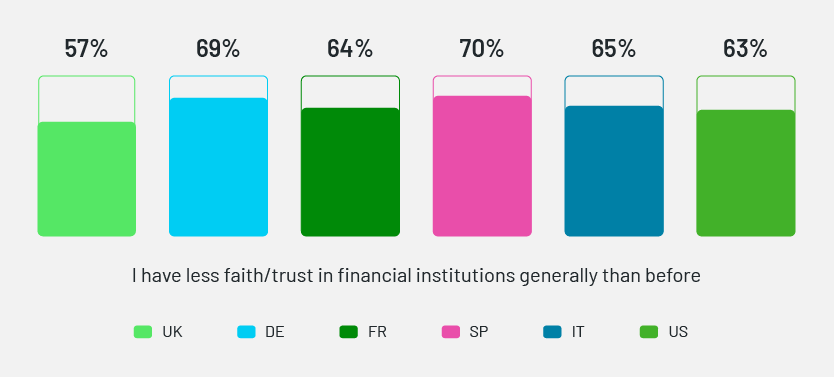

How Rising Rates Are Shaping Financial Decisions and Trust

Higher mortgage rates aren’t just stretching budgets, they’re also shaking trust in financial institutions, with 60% to 70% expressing reduced confidence. And honestly, who can blame them? When rates go up, so do frustrations.

This dip in trust could be a wake-up call for financial institutions. If they don’t step in to reassure customers, people may start looking elsewhere for financial solutions.

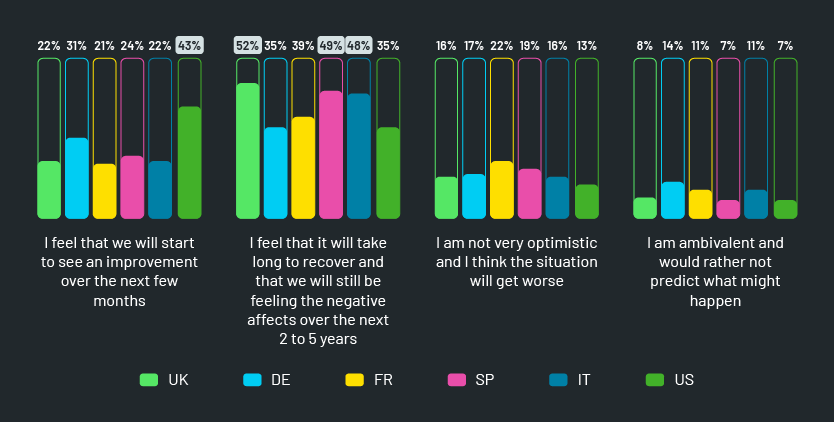

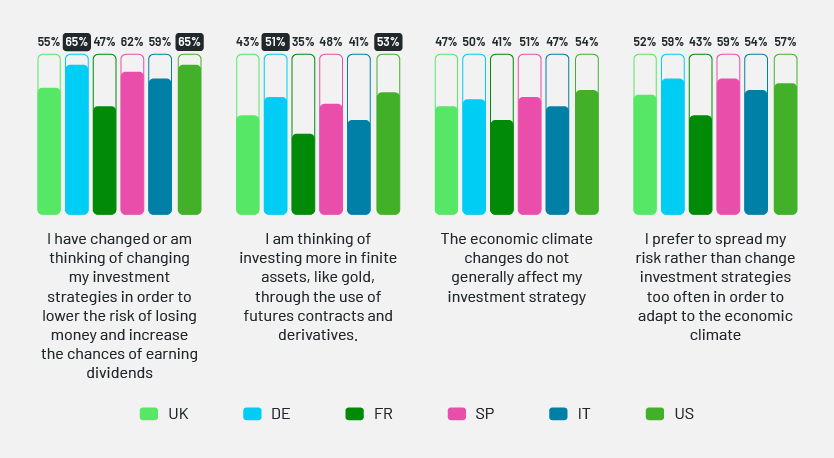

Looking to the future, most mortgage owners believe that the situation will take a while to recover and that the effects will be felt up to 5 years from now (especially amongst UK and Italian citizens). Of all markets, the US seems to be the most positive regarding a quicker turnaround.

With trust declining and financial strategies evolving, rising rates are leaving a lasting impact far beyond mortgage payments. Many are contemplating changing their investment strategies to earn more dividends and lower the risk of losing money. Some feel the need to invest in more finite assets (especially in Germany and the US), whilst others again still prefer to spread their risk rather than change strategies.

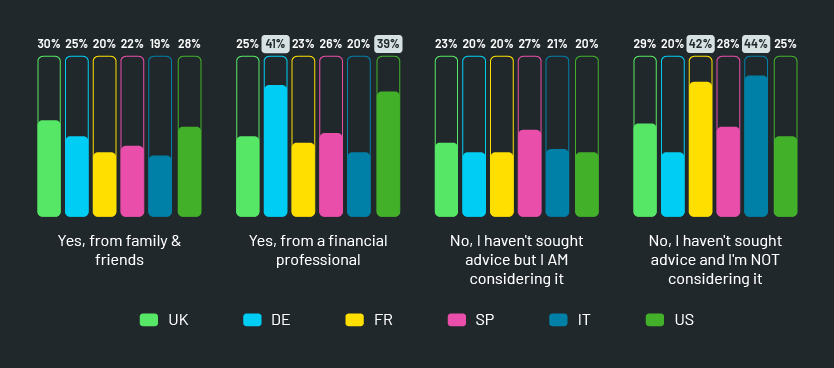

Where Do Homeowners Turn for Help with Rising Rates?

When mortgage rates climb, some people call in the experts—others just ride it out. Mortgage owners across the markets have reacted quite differently when it comes to seeking advice to assist them in managing rising mortgage rates.

In Germany and the U.S., many are turning to financial professionals for guidance. Meanwhile, French, and Italian homeowners, are not rushing to seek advice, at least not yet.

Whether it is expert advice or a wait-and-see approach, one thing is clear: homeowners are figuring out their own way to navigate this shifting financial landscape.

Why This Matters

Higher mortgage rates aren’t just a number on a loan statement— rising mortgage rates have significantly impacted people’s lives, with mental health being one of the areas most affected. Financial pressure makes it harder to stay focused on goals and maintain a positive outlook, influencing both daily decisions and future plans.

Mental Health Under Pressure

Money worries don’t just hit the wallet, they impact the mind too. Across markets, mortgage owners consistently pointed to the emotional burden of rising rates.

- It has severely affected my mental health, with not wanting to go out and do anything with friends or family just to save money and to be working constantly to make ends meet (UK)

- I’m in a constant state of worry and dread at the thought of unexpected bills as I’ve no spare cash as a result of interest rate rises (UK)

- Constant uncertainty clouds the mind. Sometimes accompanied by insomnia, sometimes by a feeling of powerlessness. (DE)

- Anxiety about taking too little and not being able to save anything for possible emergencies (IT)

Emotional discomfort, because it has risen so much that I have had to work many more hours than usual. (SP)

Rethinking Financial Futures

With so much uncertainty, homeowners are making big shifts in how they plan for the future. Savings have become a top priority, particularly in France, while others are rethinking their investment strategies. Some want to diversify their risk, while others lean toward finite assets like property or gold to feel more secure.

- Continual worry & stress from dealing with increases in my financial obligations. The future of managing my mortgage payments is uncertain. This has a detrimental impact on my daily life and my ability to plan ahead for the year. My mental and physical wellbeing have been grossly affected. I can no longer afford even a low cost gym membership (UK)

- It just makes you sick because you constantly have the feeling that you have to rethink everything (DE)

- Rising mortgage and interest rates have made managing daily expenses more difficult, increasing anxiety about the future and forcing me to review my financial plans and priorities. (IT)

- It has left us with less financial liquidity, and we have had to adapt our expenses so as not to have to take out more loans. (SP)

Achieving financial stability has become an uphill climb, almost unattainable. (SP)

Increased Spending Vigilance/Adjusted Lifestyles

For many, the first instinct is to tighten the budget—not just on luxuries, but on everyday essentials. Across markets, people are scaling back on travel, dining out, and even basic household expenses.

- Reduction in leisure and discretionary spending (social activities, travel, and vacations)

- Reduction in daily expenses (Heating and energy usage, water consumption, food purchases)

- Letting go/postponing major purchases and investments (vehicles, property, assets, and other investments)

- Adjustments that have affected their quality of life with increased stress levels affecting their daily well-being

- It makes me worried about my financial future and encourages me to be more vigilant about my money (UK)

- You have to rethink every purchase; you can’t just treat yourself like that anymore (DE)

- This encourages us to pay much more attention than before, and to watch the prices more closely. (FR)

- It has meant a reduction in how often we can have the heating on, how often we can shower and the food we eat. All of which makes for a poorer quality of life. (UK)

- It makes me nervous. Every day brings new uncertainties, so it’s hard to adjust. (DE)

- Having to do without everything despite having a full-time job makes you think that life is no longer fun and has less meaning (DE)

- There’s an almost constant, heavy tension. (FR)

It makes me feel limited, somewhat frustrated, and sad because it has influenced my relationship with my environment and activities (I go out less, I can’t do certain activities that require payment, I travel less) it even influences my education. (SP)

Feeling Powerless in a Shifting Economy

One of the hardest parts? The feeling of having no control over what comes next. Many mortgage holders express a sense of helplessness—unsure how to regain stability in a financial landscape that keeps shifting.

- You feel insecure and left alone when it comes to your financial future (DE)

- We are surviving and not living (IT)

- I am apathetic, sad, I have a feeling of ruin (SP)

Strategies for Brand Success

Rising mortgage rates aren’t just numbers on a statement—they are shaping how people spend, save, and even how they feel about the future. Our latest omni study highlights just how much these financial shifts are impacting everyday life. And here’s the thing: brands and financial institutions have a real opportunity to step up and make a difference.

Market research helps businesses and institutions stay connected to what people need and find better ways to navigate an uncertain future.

Brands play a pivotal role in consumers’ lives, especially in times of hardship, both from a financial as well as a mental well-being aspect. Insight into what consumers want and how they want brands to communicate with them, is vital right now.

Some simple strategies for brand success in these turbulent times include:

- Help consumers make smart trade-offs. Everyone is tightening their budgets, so brands that offer real value for money (think discounts, bundles, or flexible pricing) can win loyalty.

- Connect on a human level. A little empathy goes a long way. Showing that your brand understands financial pressures, whether through messaging, support programs, or even just helpful content, can build trust and connection.

- Re-emphasize the value of community, family, and the reliance on brands to ease the stresses of everyday life. Taking the ‘hardship’ out of ‘hard,’ can lighten the pressure being felt by consumers.

- Offer flexible financial solutions. Whether temporary relief programs, payment flexibility, or bridge financing, giving consumers a way to manage short-term pressures can earn long-term loyalty.

- Stay on top of shifting consumer needs. The best way to support customers? Keep listening. Ongoing market research helps brands adapt to changing behaviors and expectations, ensuring they are always in tune with what matters most.

![[OnDemand] Promotions + AI: Lift Sales Without Losing Your Brand](https://sago.com/wp-content/uploads/2026/06/blake-wisz-tE6th1h6Bfk-unsplash-scaled.jpg)

![[OnDemand] Why You Should Develop a Data Quality Tech Stack](https://sago.com/wp-content/uploads/2022/09/Single-Sign-On-Methodify.jpg)